Nigeria missing in 2024 frontier exploration programmes __Rystad

Sopuruchi Onwuka

Nigeria which has the most developed petroleum exploration and production plays in Africa is missing in new exploration drilling campaigns mapped by world’s biggest operators in the continent; highlighting the persisting investment apathy by distraught players protesting stringent fiscal conditions in the business environment.

According to industry consultancy firm, Rystad Energy, whereas Africa and Latin America will spearhead high-impact oil and gas drilling activities, the big names in African oil and gas production-Nigeria, Libya and Angola-will not host significant wild cat or high-impact exploration campaigns.

The industry consultancy stated that a combination of factors, including the size of the prospect, whether they would unlock new hydrocarbon resources in frontier areas or emerging basins and their significance to an operator’s strategy classify exploration drilling as high-impact.

According to the advisory firm, 16 (44%) of the total wells planned will be drilled by multinational oil and gas majors including BP, Chevron, Eni, ExxonMobil, Shell and TotalEnergies typically dominate high-impact well drilling, which will continue in 2024.

It stated that TotalEnergies plans five high-impact wells, Shell three, and Chevron, Eni and ExxonMobil targeting two each. It added that most drilling will be undertaken in the Atlantic margin and Asian waters with national oil companies (NOCs) and internationally focused NOCs (INOCs) accounting for eight or 22% of planned wells, upstream operators responsible for 17%, and smaller operators for the remainder.

Around 70% of African wells will be drilled in frontier and emerging basins or will open new plays, Rystad stated; adding that the important frontier wells include in the Red Sea offshore Egypt, in the Angoche Basin offshore Mozambique and in the Namibe Basin offshore Angola.

The Rystad report did not make any significant mention of Nigeria despite hopes that change in government might rekindle investors confidence in deepwater exploration.

High-impact drilling in the Americas will be primarily focused on Latin America and dominated by wells that hold significance for each operator’s long-term goals rather than frontier basins. Only two of the 12 wells planned in the Americas are in North America, with one each in the US and Canada. In Latin America, a frontier well planned for offshore Argentina would be the first drilled well in the Argentine Basin. ExxonMobil also plans to drill a frontier well in the Orphan Basin offshore Canada.

A total of six high-impact wells are planned in Asia this year, including ultra-deepwater offshore drilling in Indonesia and Malaysia, the opening of India’s Andaman Basin and a potentially resource-rich well offshore China.

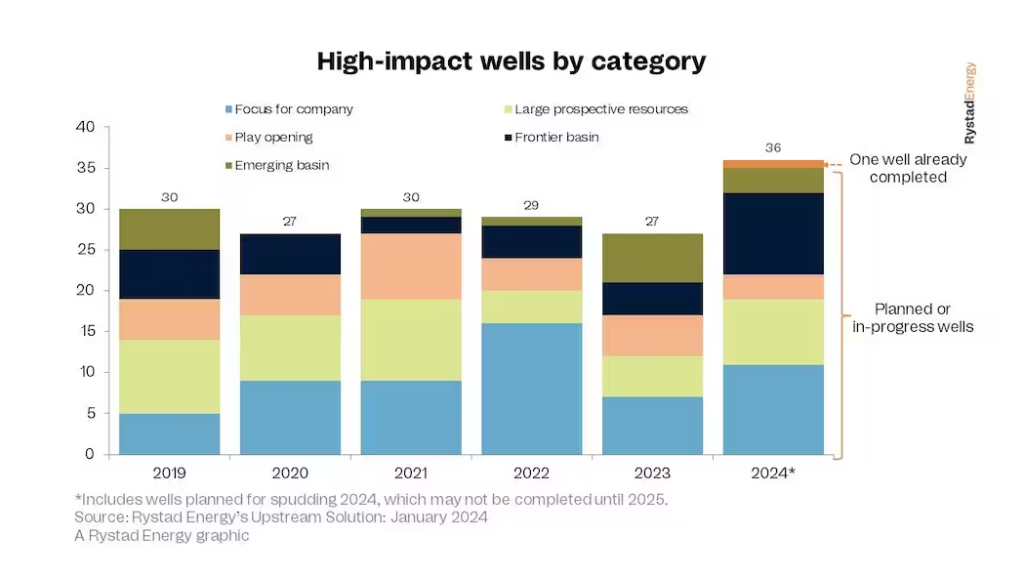

Rystad reported that the upstream industry hopes 2024 can be a bounce-back year for high-impact oil and gas drilling after a lackluster 2023, with Africa and Latin America likely to spearhead activities. Rystad Energy has identified 36 potential high-impact wells to be drilled or spud in 2024, the highest annual total since we started tracking the market in 2015. This would be a sizeable jump from the 27 high-impact wells drilled last year, and operators will hope for a better success rate.

Of these 36 potentially significant wells, 13 are in Africa and 10 in Latin America, accounting for almost 64% of the global total. Explorers will drill six of these in Asia, two each in the Middle East, Europe and North America and one in Oceania, with TotalEnergies’ planned exploration in Papua New Guinea.

Only eight of the 27 high-impact wells drilled in 2023 resulted in commercially movable volumes, a success rate of less than 30%, well below the annual average of 42%. These wells discovered volumes of 1 billion barrels of oil equivalent (boe), a sharp decline from the 3.5 billion boe found in 2022. These high-impact wells accounted for 20% of the 5 billion boe discovered by all exploration activities globally last year. To make matters worse, 2023 was an expensive year, with drilling costs rising due to a significantly tighter rig market than in prior years, worsening the blow of a low success rate.

Rystad Energy classifies high-impact wells through a combination of factors, including the size of the prospect, whether they would unlock new hydrocarbon resources in frontier areas or emerging basins and their significance to an operator’s strategy.

“Despite disappointing results in 2023, the exploration industry remains confident that fortunes can turn around this year. Drillers are still investing in frontier, emerging and play-opening areas to find volumes, but they are more targeted in their exploration strategies. Companies are deprioritizing any short-term pay-off in favor of multi-year plans and focusing on wells that best fit their long-term vision. This is a fundamental shift in the market and is unlikely to change even if 2024 success remains muted,” says Taiyab Zain Shariff, vice president of upstream research at Rystad Energy.

Of the high-impact wells planned this year, 14 will be drilled in frontier and emerging basins, with three opening up new plays entirely. So, despite a disappointing 2023, many operators continue exploring new plays and focusing on frontier regions. Eight planned high-impact wells target prospective offshore resources of more than 430 million boe and considerable prospective onshore resources of more than 230 million boe. The remaining 11 wells are strategically relevant for their respective operators, meaning exploration success would help them gain traction in the region or inform future operational decisions. If all planned wells proceed as scheduled, 2024 would see the highest number of high-impact wells drilled in at least 10 years, since we started tracking these wells in 2015.